Stablecoins have moved from a crypto-policy-side market to Kevin Warsh’s Federal Reserve’s dollar-policy agenda.

Fed Governor Christopher Waller used the central bank’s June 22 dollar conference to frame digital assets, including stablecoins, as part of the research agenda around the dollar’s international role.

The remarks were a research signal rather than a new stablecoin policy. They changed the context: stablecoin flows now sit alongside dollar funding, payment rails, cross-border capital movement, safe-asset demand, and the question of how private token issuers touch public dollar infrastructure.

That reframes the market. Dollar-backed stablecoins are still crypto trading tools, payment tokens, and regulatory objects. The Fed’s dollar agenda now treats them as a possible transmission channel too.

Waller’s remarks and the Fed’s conference agenda place them within a larger system: private digital-dollar claims that can move across exchanges, wallets, issuers, banks, and reserve portfolios, while still relying on the U.S. dollar and the short-term assets backing it.

The reasonable question is what changes if those issuers become one of the channels through which global demand for dollars reaches the banking system and the Treasury market.

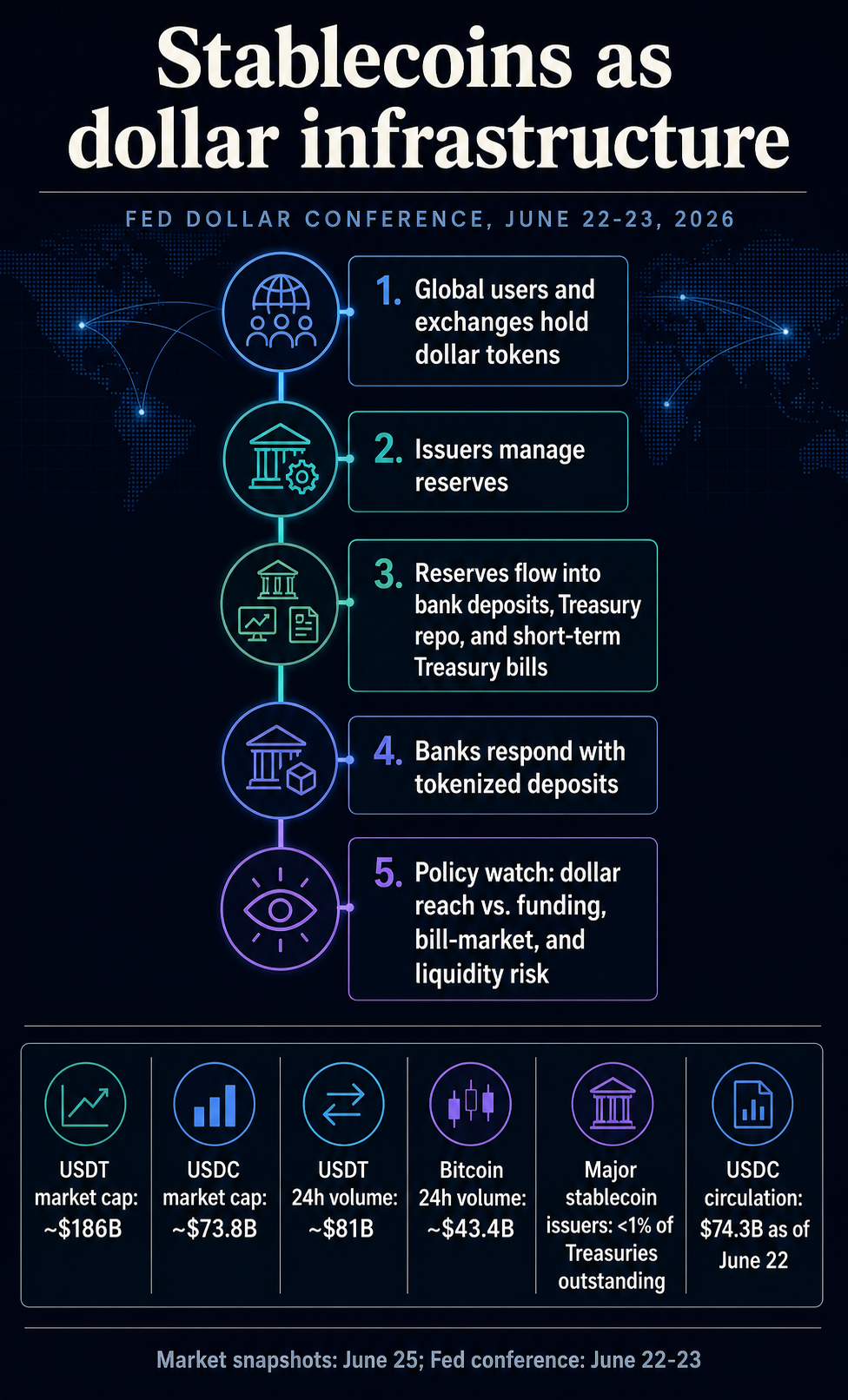

The Fed is treating stablecoins as dollar rails

Waller’s welcoming remarks at the Fifth Conference on the International Roles of the Dollar described distributed-ledger technologies and tokenized assets, including stablecoins, as creating channels for global dollar intermediation alongside, or in connection with, traditional banks and payment systems.

The conference agenda clarifies the policy frame. The Fed and the New York Fed organized the June 22-23 event around financial innovation, digital assets, the dollar’s roles in investment and payments, market structure, reserve-currency status, digital fragmentation, and geopolitics.

Stablecoins sit inside that wider digital-dollar research map, alongside other digital-asset and market-structure questions.

The dollar’s role is usually discussed in terms of banks, Treasury markets, foreign reserves, trade invoicing, and offshore funding. Stablecoins add a private technology layer to that map.

A user outside the United States can hold a dollar-denominated token, move it across blockchains, trade it against other assets, or redeem it through an issuer while interacting with the dollar system in a different way from a bank depositor or money-market-fund investor.

The result is a more complicated form of dollar access. Stablecoins can extend dollar reach by making dollar claims easier to hold and transfer.

They can also pull private issuers into policy debates once reserve management, redemptions, liquidity shocks, or offshore demand become large enough to affect other markets.

This is why scale changes the policy problem. Stablecoins remain small compared with the full Treasury market, yet they are already large within crypto.

CryptoSlate market data showed Tether and USDC among the five largest crypto assets by market capitalization, with USDT at nearly $186 billion and USDC at nearly $73.8 billion on June 25.

Tether’s 24-hour volume alone was around $81 billion, nearly double Bitcoin‘s roughly $43 billion in the same market view.

Those figures are only one point in time. The larger point is that dollar tokens now have enough scale and turnover to prompt central-bank researchers to ask where the dollars behind them come from, where reserves are held, what happens during redemptions, and whether the flows create pressure in places that were previously studied mostly through banks and money funds.

Circle’s own materials put USDC in circulation at $74.3 billion as of June 22 and describe the token as backed by highly liquid cash and cash-equivalent assets. Circle also says most of the reserve is held in the Circle Reserve Fund, an SEC-registered government money market fund managed by BlackRock.

That kind of structure turns a payment token into a reserve-management channel. A change in stablecoin demand can change demand for bank deposits, Treasury repo, or short-term Treasury bills, depending on how the issuer manages backing assets.

The dollar-policy narrative, therefore, goes beyond one-to-one redemption. The policy issue is whether enough private tokens, backed by sufficient short-term dollar assets, can be integrated into the distribution and absorption of dollar liquidity.

Stablecoins compete for both payments and balances

Fed staff research has already begun to separate potential bank effects from the simpler claim that stablecoins drain deposits. A May FEDS Note said stablecoins are notable because they combine balance-holding and payment functionality on digital rails, meaning they compete for both transaction balances and payment flows.

A separate Fed note from December described the deposit impact as conditional. Stablecoin growth may reduce, recycle, or restructure bank deposits depending on who demands the tokens, what assets they convert, and how issuers hold reserves.

Domestic users moving transaction balances out of banks would have one effect. Offshore users seeking digital dollars could have another.

Issuers parking reserves in banks, money funds, repo, or bills would transmit the growth through different parts of the financial system.

Banks are now part of the response. The Clearing House announced on June 5 that major financial institutions are backing an on-chain commercial-bank-money initiative to support tokenized deposit clearing and settlement while connecting blockchain activity to RTP and CHIPS.

The announcement shows the direction of the bank response: keep digital money movement inside regulated commercial-bank money as stablecoins build always-on dollar rails.

A 2026 New York Fed staff research report argued that stablecoin activity can transmit liquidity stress to banks and complicate monetary-policy implementation.

That is not an official policy statement, but it points to the same issue Waller’s conference framing raised: once stablecoins interact with banks, reserves, and wholesale payments, their effects can leak out of crypto markets.

The strongest macro link is short-term safe-asset demand. A June BIS working paper found that dollar-backed stablecoin inflows can lower short-term Treasury bill yields, with effects that intensify during Treasury market stress and as the sector grows.

The paper’s finding is fairly specific: it describes yield compression from inflows at short tenors, with no claim about the full Treasury curve.

Treasury advisory materials add the scale check. A 2026 Treasury Borrowing Advisory Committee presentation found that major stablecoin issuers hold less than 1% of outstanding Treasuries.

The same presentation also said stablecoins could increase demand for short-end Treasury issuance if future growth comes from new offshore dollar demand. That combination is the tension policymakers have to track.

Today, stablecoins can be small relative to the full Treasury market and still affect bills and repo at the margin.

On a larger scale, their reserve portfolios could become another source of demand for the safest and most liquid dollar assets. During stress, redemptions could work in the other direction.

The dollar-reinforcement argument depends on this channel. If dollar stablecoins continue to spread abroad, they can expand access to dollar instruments without requiring a foreign user to have a U.S. bank account.

But that also means private issuers and reserve managers become part of the distribution system for dollar liquidity. The more successful the model becomes, the harder it is to treat it as a crypto side market.

The next signal is how the system absorbs them

The Fed’s June conference leaves open whether stablecoins will remain a tolerated private extension of dollar dominance or become a more explicitly regulated layer of dollar infrastructure. It shows that the question has moved into the dollar’s main research agenda.

The near-term signals suggest policymakers will watch whether stablecoin growth is driven by offshore dollar demand or domestic substitution from bank deposits.

Banks will test whether tokenized deposits can match the speed and programmability of stablecoins while keeping balances within the banking system. Issuers will have to demonstrate that reserves, redemptions, and concentration risks can withstand rapid expansion or contraction in stablecoin supply.

That is what changes when the Fed treats stablecoins as part of global dollar transmission. A token that once looked like crypto’s settlement asset becomes a private dollar rail with public consequences.

Its growth can support dollar reach, but it can also raise questions about bank funding, Treasury-bill demand, and liquidity stress in the same frame.

The threshold is lower than replacing banks or dominating Treasury markets. Stablecoins become a policy problem once they are large enough, useful enough, and connected enough that dollar demand increasingly passes through them.

The post Stablecoins are quickly becoming the Kevin Warsh’s Fed’s next policy problem appeared first on CryptoSlate.