Mark Cuban sold most of his Bitcoin because it failed to provide a hedge when fiat confidence weakened and geopolitical risk rose.

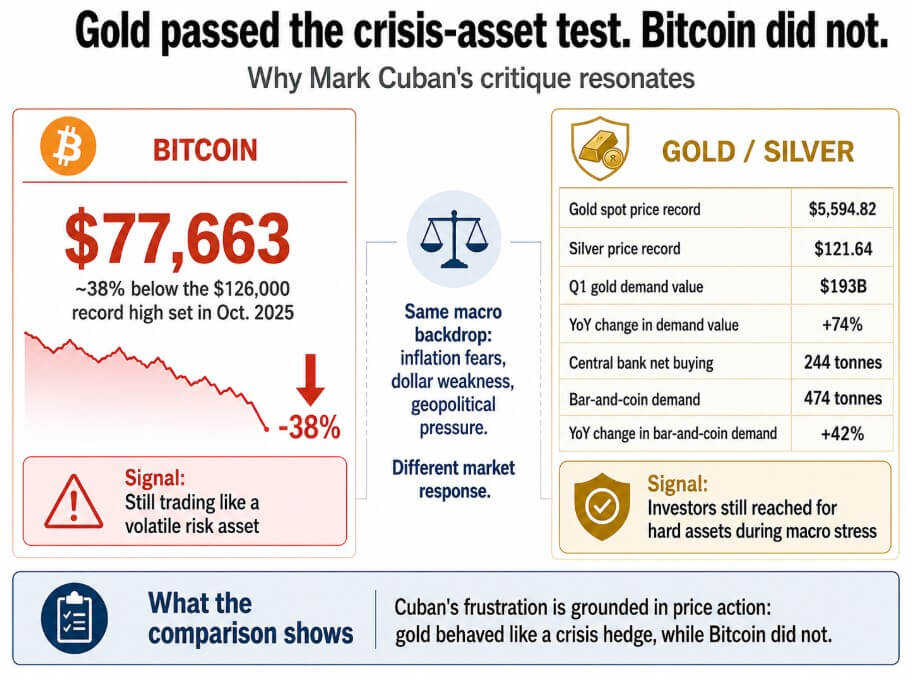

Cuban called it “not the hedge I expected it to be,” and the price record supports his frustration. Bitcoin traded around $77,663 in mid-May 2026, roughly 38% below the record high of $126,000 set in early October 2025.

Spot gold hit a record $5,594.82 on Jan. 29, while silver touched $121.64 the same day, driven by the same macro variables Cuban cited: inflation fears, dollar weakness, and geopolitical pressure.

World Gold Council data shows that gold demand in the first quarter reached 1,231 tonnes, including OTC, and the dollar value of quarterly demand jumped 74% year over year to a record $193 billion.

Central banks bought 244 tonnes net in the same period, and bar-and-coin demand hit 474 tonnes, up 42% year over year. Cuban also told Portfolio Players he is moving more money into Ethereum than Bitcoin, but the hedge critique is specific to Bitcoin.

The ‘digital gold’ pitch always had a problem

Bitcoin.org describes the asset as peer-to-peer money with no central authority or banks and specifies that issuance halves over time, eventually stopping at 21 million Bitcoin. Nothing in that description commits Bitcoin to rising when geopolitical stress rises.

Cuban built a thesis on the “digital gold” narrative that the market constructed and the Bitcoin whitepaper never endorsed.

Bitcoin has traded as a liquidity-sensitive, high-beta asset that correlates with the Nasdaq during risk-off episodes and surges when risk appetite returns.

Last year, crypto moved with broader equities through the April tariff shock before Bitcoin hit its October record, then suffered a major leverage wipeout. More recently, Glassnode’s May 20 report describes Bitcoin as structurally resilient but notes that spot demand has weakened, ETF accumulation has slowed, and options positioning has turned defensive.

Cuban applied a gold benchmark to an asset that has never consistently moved like gold, and the resulting distance between what he expected and what the price did is what drove him to sell.

| Test | Gold | Bitcoin |

|---|---|---|

| Crisis behavior | Cleaner panic shelter | Often sells off with risk assets |

| Volatility profile | Lower, more established | Much higher, adoption-sensitive |

| Main demand driver | Inflation fear, geopolitics, central banks | ETF flows, liquidity, regulation, leverage cycles |

| Monetary property | No issuer, physical scarcity | 21M cap, no central issuer, permissionless transfer |

| Best framing | Crisis shelter now | Monetary optionality later |

Bitcoin long-term holder supply rose by over 2 million BTC during the current drawdown, reaching 16.3 million BTC, with roughly 200,000 BTC added in the past month alone. Cuban is judging Bitcoin by whether it acts like gold in a crisis, while long-term holders are judging it by whether the network still functions and the supply cap holds ten years from now.

A hedge reduces portfolio risk during stress events with some consistency, but Bitcoin’s realized volatility runs far above gold’s, its price responds to ETF flows, regulatory headlines, and leverage cycles, and it has repeatedly correlated with equity drawdowns during acute stress.

Those are the mechanics of an early-stage monetary network still pricing in adoption uncertainty, with an asset that may be powerful over a long horizon precisely because it is too volatile and too liquidity-sensitive to function as a short-term panic hedge.

Investors reach for Bitcoin, if the adoption thesis holds, when they expect the monetary system itself to look different in the next decade. The fixed supply, permissionless transferability, and absence of a central issuer are the properties that make Bitcoin worth considering as long-duration monetary optionality.

The distance between $58,000 and $165,000

Citi’s March 2026 forecast is a 12-month base target of $112,000, a recessionary downside of $58,000, and a bull case of $165,000, which captures how wide the resulting uncertainty runs.

Glassnode places the Realized Price near $54,900 as a lower structural boundary, while the $70,000 level carries weight as the pre-election anchor.

| Scenario | BTC level / range | Market logic | Narrative outcome |

|---|---|---|---|

| Structural floor | ~$54,900 | Realized Price lower boundary | Break below here weakens the adoption case |

| Recessionary bear case | $58,000 | Higher yields, ETF outflows, weak spot demand | Bitcoin trades like a de-risking asset |

| Key anchor | $70,000 | Pre-election reference level | Market tests whether support is real |

| Base case | $112,000 | Citi 12-month target | Bitcoin survives as volatile monetary optionality |

| Bull case | $165,000 | ETF demand, regulation, risk appetite recover | Adoption thesis absorbs the hedge failure |

In the bear case, higher yields, continued ETF outflows, and weak spot demand keep Bitcoin pinned near structural support.

Bitcoin trades like a de-risking asset, fails to distinguish itself from the broader risk-off environment, and gold continues to absorb the crisis-hedge flows that Bitcoin’s marketing promised to capture.

In the bull case, ETF demand recovers, regulatory progress in the US provides institutions with cleaner on-ramps, and risk appetite returns enough to push Bitcoin back through the $112,000 Citi target and toward $165,000.

Bitcoin survives the critique by operating as a scarce, borderless, permissionless monetary network that gains value as more institutions and sovereigns want an asset outside traditional finance.

The 21 million supply cap and the absence of a central issuer are the properties that make Bitcoin worth holding as a long-duration bet on monetary distrust becoming infrastructure, and those properties held through the same drawdown Cuban is citing as proof of failure.

Bitcoin’s actual case rests on offering exposure to a world where more people want money outside the traditional system, which holds regardless of how Bitcoin performs against gold in any given crisis.

Bitcoin as a call option on monetary distrust

Cuban wanted Bitcoin to act like a predictable and consistent protection against the specific risks he saw coming.

Yet, Bitcoin may be closer to a call option on monetary distrust: valuable if the thesis plays out over a decade, volatile in the meantime, and a poor substitute for gold during acute stress.

Gold is still the cleaner crisis asset by every recent measure, shown through record prices, record quarterly demand value, sustained central bank buying, and consistent performance against the macro variables that define genuine panic.

The asset Cuban sold most of his stake still has a 21 million supply cap, still operates without a central issuer, and still accumulated 200,000 BTC of long-term holder supply in the past month.

Whether that is enough to justify the price range of $58,000 to $165,000 over the next year depends on whether the adoption thesis can replenish what the hedge thesis has lost.

The post Mark Cuban’s Bitcoin sale tests the gap between a failed hedge and a surviving monetary bet appeared first on CryptoSlate.