BlackRock’s iShares Bitcoin Premium Income ETF has moved from launch watch to live market structure, giving Bitcoin investors a new choice: hold spot exposure directly or accept a covered-call wrapper that turns part of Bitcoin’s volatility into monthly income.

The fund, trading under the ticker BITA, began listing on Nasdaq today, June 16, after a Nasdaq listing alert named Susquehanna Securities as the designated liquidity provider.

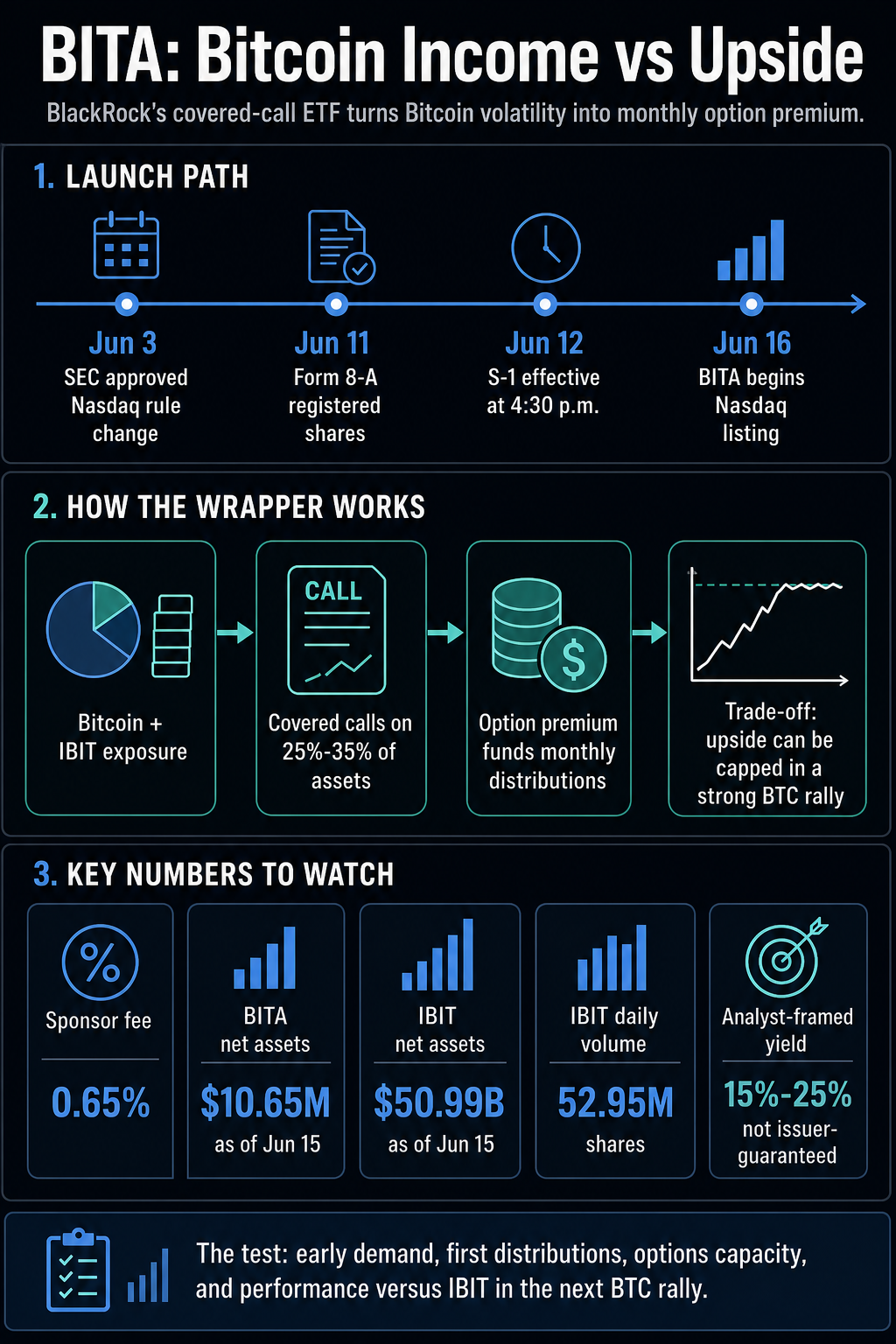

The launch path followed the SEC’s June 12 notice of effectiveness for the fund’s S-1 registration statement, a June 11 Form 8-A registering the trust’s shares under Section 12(b), and the SEC’s earlier approval of Nasdaq’s rule change to list and trade the product.

That puts BITA in a different category from a plain spot trust. The fund starts with Bitcoin exposure but packages it through an options-income overlay.

That structure turns the liquidity and volatility around BlackRock’s $50 billion-plus iShares Bitcoin Trust ETF, IBIT, into a monthly distribution strategy. The trade-off is equally important: the income comes from selling call options, which can dampen volatility in flat or moderately rising markets but can leave holders behind when Bitcoin runs sharply higher.

BlackRock moves from spot access to structured income

BITA entered the market with a 0.65% sponsor fee, monthly distribution frequency, Nasdaq listing, June 9 inception date, and $10.65 million in net assets as of June 15.

It also listed 200,000 shares outstanding as of June 15 and two holdings as of June 12.

The fund’s strategy seeks spot Bitcoin performance plus option premium income. It can hold Bitcoin and IBIT directly, then write covered calls on about 25%-35% of portfolio assets.

In practical terms, BITA is selling part of the portfolio’s upside potential in exchange for option premium that can support monthly distributions.

That structure places the product in the next stage of Bitcoin ETF design. The first phase of US spot Bitcoin ETFs solved access, custody, brokerage availability, and institutional packaging.

BITA asks whether Bitcoin’s volatility can serve as an input to income-oriented portfolios without stripping away too much of the asset’s upside.

The timing gives BlackRock a natural distribution advantage. IBIT listed roughly $51 billion in net assets and a daily volume of about 53 million shares as of June 15.

BITA is tiny by comparison at launch, but it is built around the same iShares Bitcoin ecosystem and a market where IBIT options have become a visible part of the trading stack.

| Product | Core exposure | Income method | Main trade-off |

|---|---|---|---|

| BITA | Bitcoin and IBIT exposure | Covered calls on roughly 25%-35% of assets | Monthly income potential in exchange for capped upside on overwritten exposure |

| IBIT | Spot Bitcoin exposure | Direct price participation | More direct participation in Bitcoin price moves, without an option-premium buffer |

| Goldman Sachs filing | Indirect Bitcoin ETP-linked exposure | Options overwrite expected around 40%-100% | Broader income overlay, still exposed to capped-upside and options execution risk |

That comparison is the point for allocators. BITA is a hybrid exposure tool: part Bitcoin access, part options-income strategy, and part test of whether IBIT’s scale can support a recurring distribution wrapper.

The early asset base also keeps the launch in perspective. BITA is a small wrapper at inception, while IBIT remains the distribution engine with more than $50 billion in net assets. That gap makes early volume, spreads, and monthly distribution levels more meaningful than launch assets alone.

The yield hook depends on an upside cap

The phrase “Bitcoin yield supercycle” is exciting because it captures what Wall Street is trying to build: funds that make Bitcoin feel less like a pure directional bet and more like an income sleeve.

BITA is a clear example of that shift, and its mechanics are straightforward. Option premium has to come from somewhere, and in a covered-call product it comes from selling away part of the benefit from a strong rally.

BlackRock’s issuer materials avoid promising a fixed return. The product brief says the fund seeks monthly income and aims to participate in the majority of Bitcoin’s upside, while noting that actual upside participation can vary.

The issuer’s risk language warns that covered calls can limit gains above the exercise price, while the brief says the fund may underperform IBIT when Bitcoin rises significantly.

Bloomberg ETF analyst Eric Balchunas has framed the launch around a 15%-25% annualized yield target and at least 70% upside participation, and CryptoSlate’s June 16 yield analysis repeated that market framing.

Those figures should stay separate from issuer-backed claims. The firmer BlackRock-backed facts are the monthly distribution frequency, the 25%-35% covered-call overwrite target, the 0.65% sponsor fee, and the claim that the strategy seeks majority upside participation, with actual results dependent on market conditions.

For investors, the real question is whether that cost is acceptable. In a sideways market, an option-income sleeve may seem useful because option premiums can help offset volatility while the fund still maintains Bitcoin exposure.

In a strong rally, the same structure can lag a direct spot product because a portion of the upside has already been sold.

The risk stack also goes beyond the headline yield figure. BITA still depends on Bitcoin’s price path, IBIT liquidity, options execution, tax treatment, and whether distributions come from repeatable premium capture or from a market environment that later changes.

A monthly payout can make exposure easier to fit within an income portfolio, while total return relative to IBIT through both rallies and drawdowns will determine whether the wrapper earns its fee.

The market test starts with demand and distributions

The launch advances a story CryptoSlate has already tracked. June 11 coverage followed the BlackRock and Goldman Sachs race to package Bitcoin volatility into premium income, while the broader June 16 analysis placed BITA inside the push to normalize Bitcoin yield strategies.

BITA’s listing shifts that debate from filing language into observable market behavior.

Goldman’s pending filing for a Bitcoin Premium Income ETF shows the category is still being tested rather than standardized. The registration filing describes a strategy with indirect Bitcoin exposure and a much larger expected overwrite range of around 40%-100%.

That contrast shows Wall Street trying different ways to package volatility, option liquidity, and investor appetite for distributions.

The market backdrop makes the pitch easier to understand. Bitcoin is trading around the mid-$66,000s, up over seven days but down over 30 days, while broader CryptoSlate market data showed Bitcoin dominance near 58.6%.

That mixed trend is exactly the type of market where income wrappers get attention: investors may still want Bitcoin exposure while seeking a way to be paid during consolidation.

The risk is that income language can soften the perception of how much risk remains. BITA still depends on Bitcoin, IBIT, options execution, tax treatment, liquidity, and the path of future price moves.

Its distributions will only answer part of the question unless investors can see how much return came from premium, how much came from underlying Bitcoin exposure, and how much upside was given away in a rally.

That is the test from here. Early trading volume will show whether investors want a Bitcoin income wrapper from BlackRock at scale.

The first monthly distributions will show how the strategy looks in dollar terms. Options-market capacity will show whether the approach can grow beyond a launch product.

The next strong Bitcoin rally will show whether BITA’s income feels like a useful volatility harvest or an expensive way to make BTC exposure look like yield.

The post BlackRock’s new Bitcoin ETF offers monthly income, but caps gains when Bitcoin surges appeared first on CryptoSlate.