Options traders are building bearish positions around Strategy’s (formerly MicroStrategy) flagship preferred STRC stock after the security fell to a record low, adding a new layer of pressure to one of Michael Saylor’s main funding tools for buying Bitcoin.

Strategy’s Variable Rate Series A Perpetual Stretch Preferred Stock, known by the ticker STRC, closed Wednesday at $89 after touching an intraday low of $88.51.

The close left the security about 11% below its stated $100 level and extended its year-to-date decline to roughly 10.7%.

The move is drawing added attention because STRC was designed to trade near $100 through monthly dividend adjustments.

Instead, the preferred stock is now trading near levels that imply investors want a higher payout for holding it, while options activity shows traders leaning toward further downside.

STRC options traders take bearish positions

OptionsCharts data for STRC contracts expiring June 18 showed total put open interest of 8,951 contracts, compared with 7,906 call contracts.

That put-call open interest ratio of 1.13 is modestly bearish, but the concentration of activity is more telling. The open interest in puts stood at 1,912 contracts at the $60 strike, 1,230 at the $80 strike, and 916 at the $85 strike.

The same data showed a max-pain level of $95, above STRC’s close, while net gamma exposure stood at-$1.1 million per 1% move. Negative gamma can lead dealers to hedge in ways that amplify price swings when an asset moves lower, though the effect depends on trading flows and market depth.

This option setup indicates that traders are monitoring whether the discount to par becomes persistent enough to force a change in Strategy’s dividend policy or to slow its use of STRC as a BTC funding vehicle.

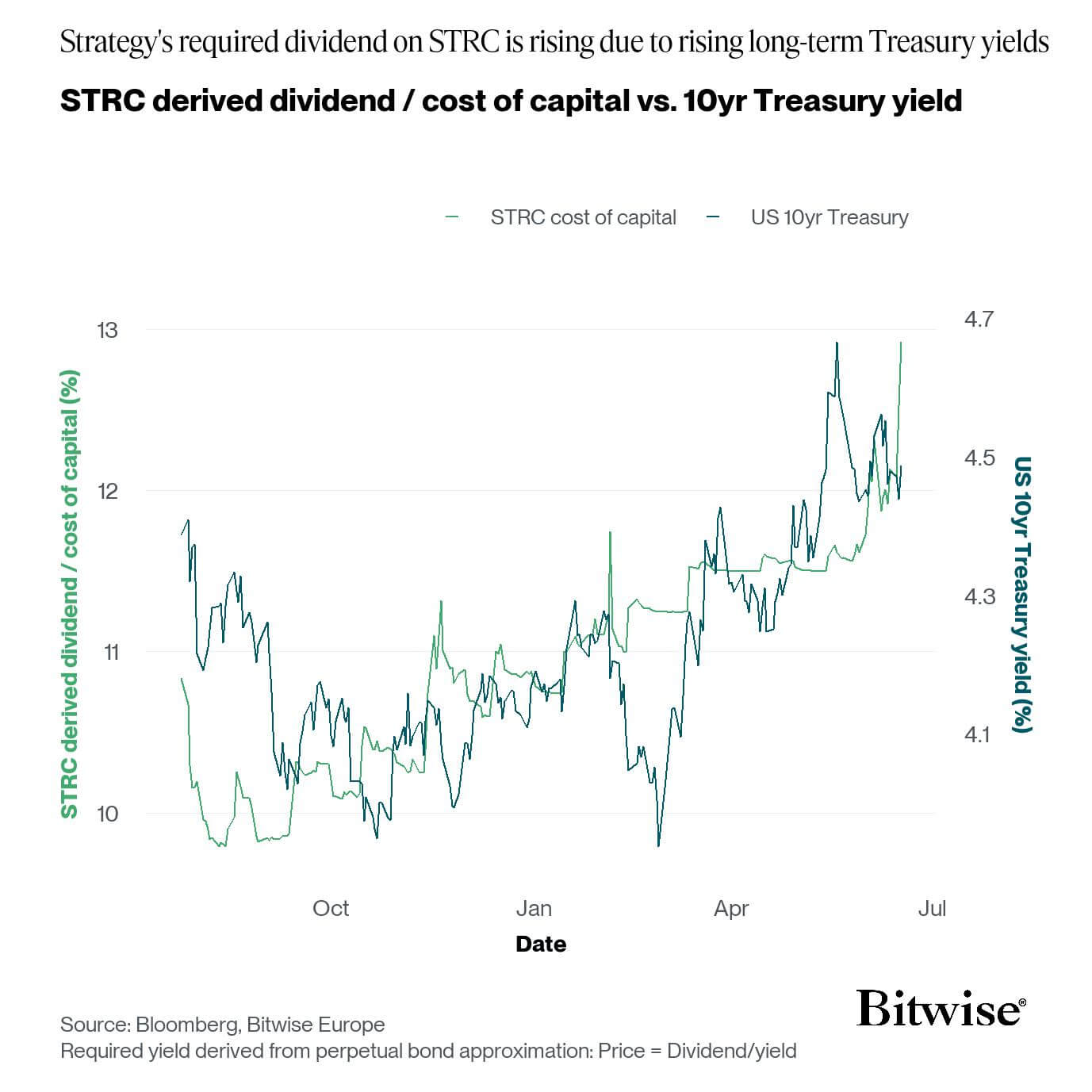

Andre Dragosch, head of research at Bitwise Europe, said STRC’s weakness suggests that Saylor may need to raise the dividend or the broader rate environment may need to ease before the preferred stock can return to $100.

He estimated that a dividend closer to about $13 annually, or roughly 13% of the stated amount, would be needed to restore the stock to par under current conditions.

That creates a difficult trade-off. Raising the dividend could support STRC’s current price action and reopen the issuance channel, but it would also increase Strategy’s cash obligations.

On the other hand, leaving the dividend unchanged could preserve near-term cash costs, but it risks letting the discount widen further.

Strategy’s dividend runway comes under scrutiny

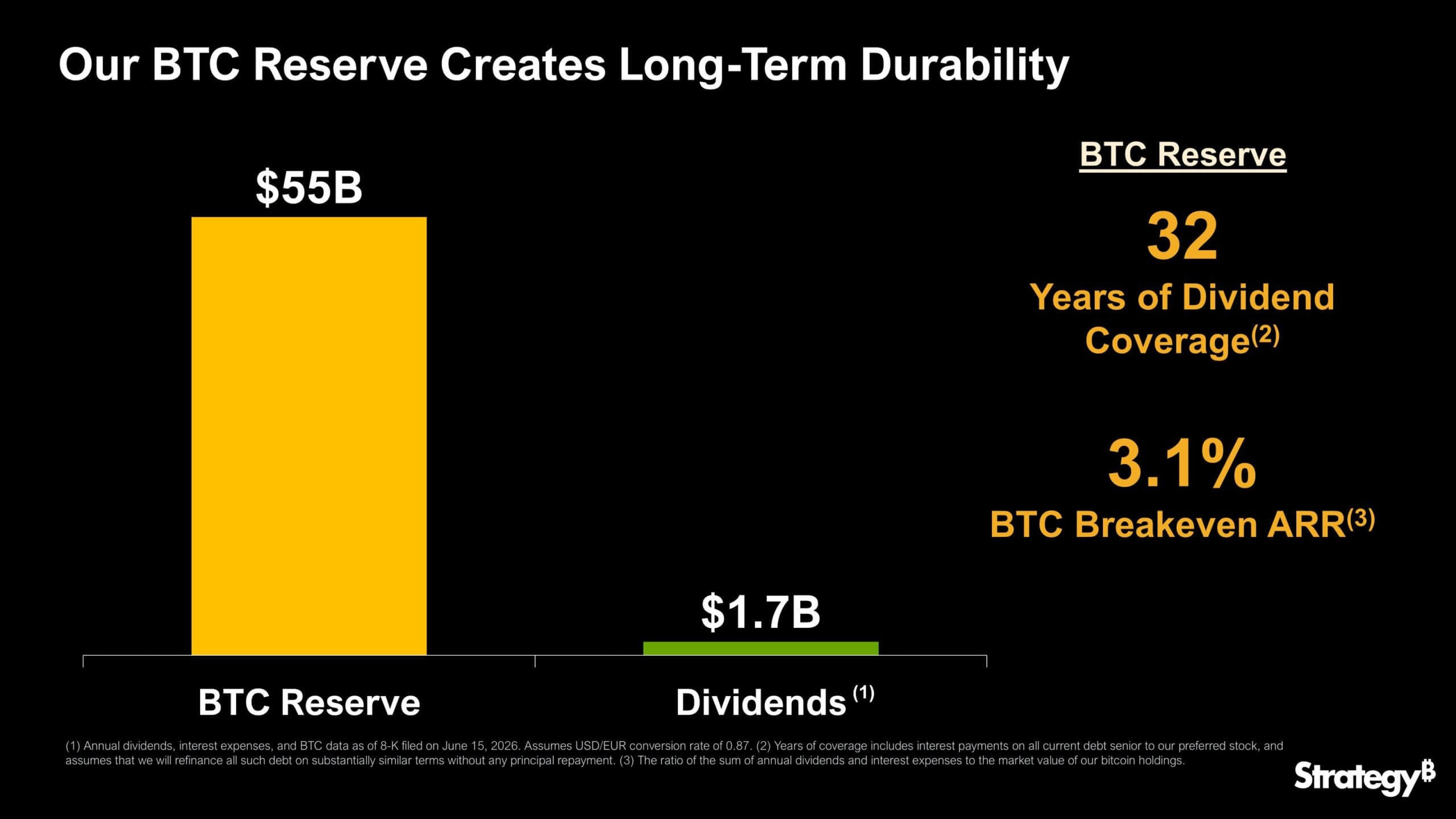

Strategy has sought to ease concerns over STRC by pointing to the size of its Bitcoin holdings, saying its reserves provide 32 years of dividend coverage. The company holds 846,842 BTC, worth about $54.2 billion at recent prices, making it the largest public holder of the cryptocurrency.

On paper, the coverage claim remains intact. Strategy’s Bitcoin treasury is worth just under $55 billion, compared with about $1.7 billion of annual preferred-dividend obligations. However, that calculation depends heavily on Bitcoin’s market price and does not answer the cash-flow question now facing investors.

CryptoQuant analyst JA Maartunn said:

“If Strategy had to sell BTC to cover those dividends, it would create selling pressure that could push BTC prices lower. That, in turn, would reduce the value of its BTC reserves and shorten the very dividend coverage it’s highlighting. In other words, if sustained, it risks becoming a downward spiral.”

Indeed, the sensitivity of that claim has already become clear. Last November, Strategy claimed it had 71 years of dividend coverage, assuming Bitcoin’s price stayed flat. But since then, Bitcoin’s price has halved, and the estimated coverage period has since fallen sharply.

That does not mean Strategy is close to exhausting its assets. The company still holds a large Bitcoin position and has raised cash by selling common stock.

However, the market’s concern has shifted from asset value to liquidity. Preferred dividends must be paid in cash when declared, while Strategy’s Bitcoin holdings fluctuate with the market and are not pledged as direct collateral to STRC investors.

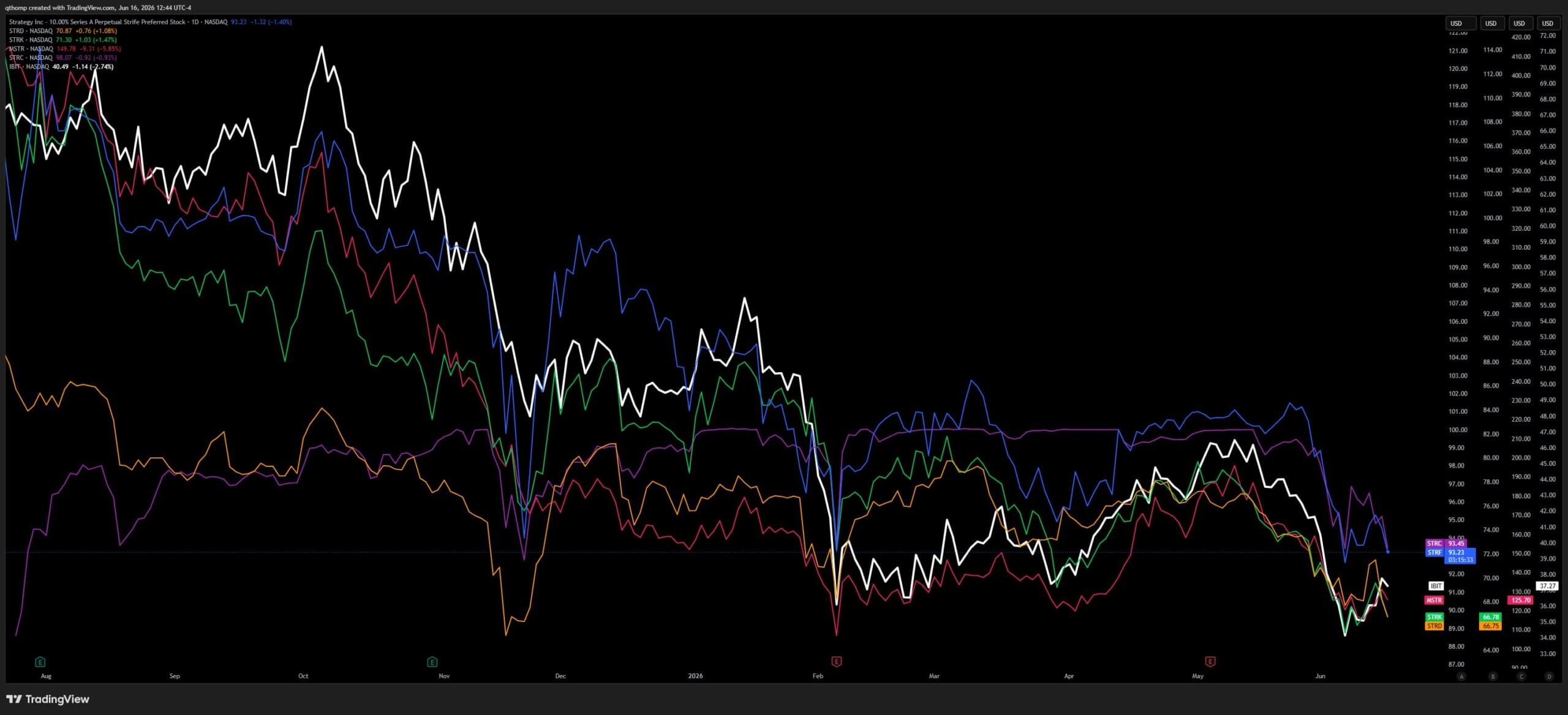

Quinn Thompson, chief investment officer of Lekker Capital, said pressure across Strategy’s capital structure is likely to persist until the company strengthens its balance sheet and improves liquidity.

According to him, the weakness has extended beyond STRC, suggesting investors are reassessing the company’s broader financing model rather than a single preferred security.

Singapore-based crypto trading firm QCP said Bitcoin’s recent underperformance partly reflects those concerns. Bitcoin has remained below $65,000 even as broader risk assets have traded higher, with traders watching whether Strategy may need to sell more Bitcoin or issue additional MSTR shares to support its preferred-stock obligations.

QCP said Strategy’s repurchase of $1.5 billion of 2029 convertible senior notes, followed by fresh common-stock sales, has added to the overhang.

The company has raised about $200 million through MSTR sales and continued to buy Bitcoin with the proceeds, but investors remain focused on how long its cash runway can support dividend payments without adding pressure to its capital structure.

The post Strategy’s STRC draws bearish options bets as it falls to new all-time low appeared first on CryptoSlate.