24X National Exchange’s latest tokenized stock filing has put Wall Street’s core plumbing at the forefront of the equity-tokenization race.

The exchange filed SR-24X-2026-20 on June 11, with the SEC issuing its notice on June 16 and the June 22 notice placing the filing in the Federal Register.

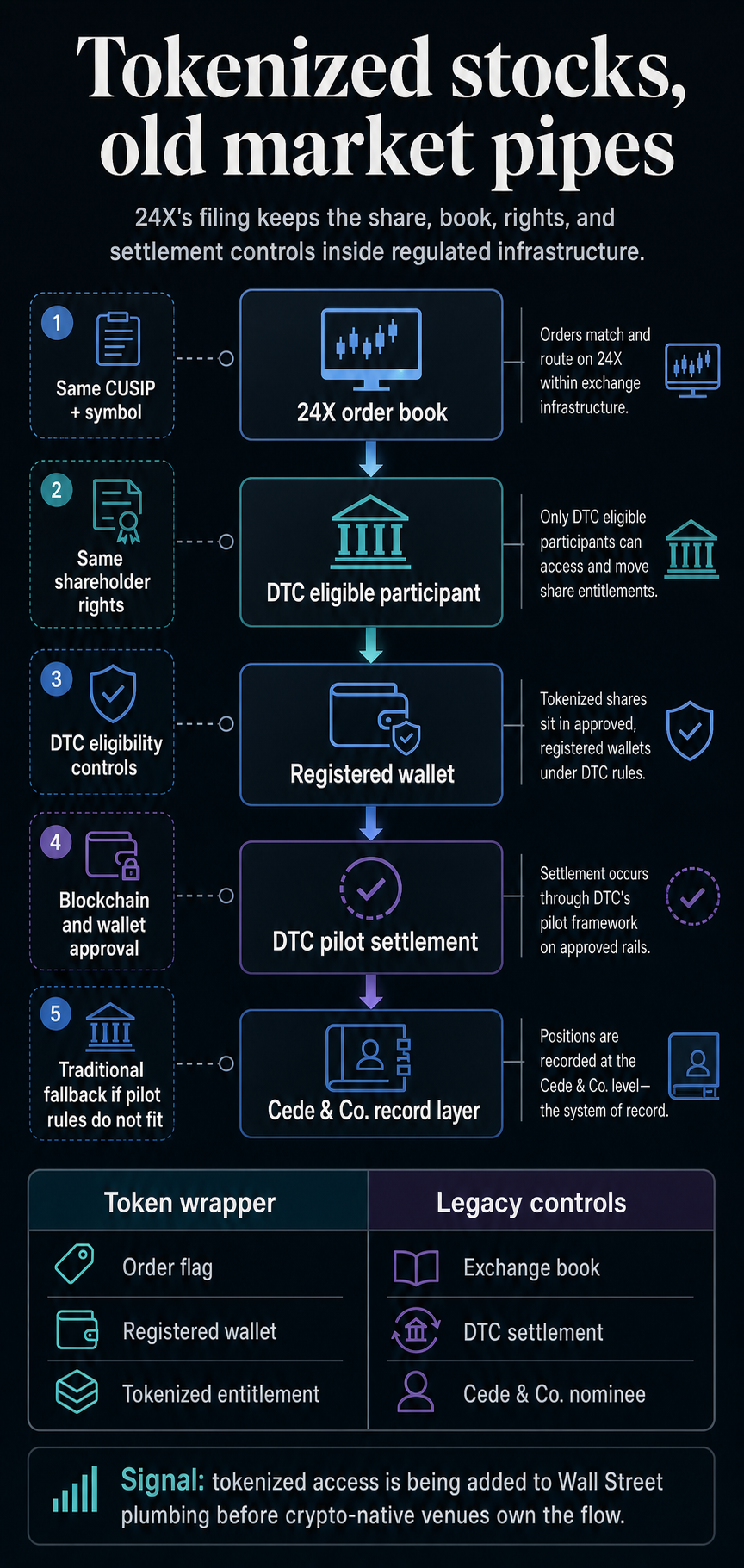

The rule change would let eligible 24X members trade certain securities in tokenized form during a Depository Trust Company pilot, according to the SEC’s notice filing.

The filing frames tokenization as an upgrade to the national market system rather than a workaround. The model described by 24X keeps the exchange, DTC, participant eligibility, order-entry controls, and shareholder-rights protections in place.

The token layer changes how eligible positions can be represented and settled, while the legal identity of the share and the market structure around the trade stay intact.

The filing’s answer is practical: tokenized stocks look like legacy market infrastructure adding a token wrapper.

The token layer stays inside the market system even with tokenized stocks

The filing would amend 24X rules covering eligible securities, member access, order priority, and routing. The proposed structure would allow DTC Eligible Participants to trade tokenized versions of eligible equity securities and exchange-traded products on 24X during the DTC pilot.

The SEC notice says the securities would trade within the current national market system, using DTC to clear and settle trades in token form based on instructions selected when orders are entered.

That keeps tokenized equity activity connected to the same market architecture that governs ordinary exchange-traded shares.

24X also framed the proposal as part of an exchange-led pattern. The filing says it is based on a similar Nasdaq proposal that the SEC already approved.

The approved Nasdaq precedent shows the same DTC-compatible exchange model can extend across national securities exchanges.

That is the old-pipes-new-token-access tension at the center of the story. Crypto traders are used to thinking of tokenization as a way to move assets outside legacy intermediaries.

The 24X filing points in the opposite direction: regulated exchanges are preparing to offer tokenized access while preserving the institutions that already control exchange trading, custody records, and post-trade settlement.

| Market function | Tokenized implementation in the filing | Market-structure effect |

|---|---|---|

| Exchange trading | Tokenized and traditional versions trade on the same 24X book | Liquidity stays connected to the exchange book |

| Security identity | Tokenized shares must share the same CUSIP, symbol, rights, and privileges | The token is treated as a form of the same security |

| Clearing and settlement | DTC handles token-form settlement during the pilot | The post-trade layer remains inside regulated market infrastructure |

| Eligibility controls | Member, security, blockchain, and wallet eligibility determine whether tokenization works | Token access is permissioned and operationally constrained |

The table captures the filing’s central tradeoff: tokenization adds a new representation layer, but each essential market function remains tied to a familiar regulated gate.

The token format works only when exchange rules and DTC systems allow it.

Same stock, different form

The proposed rule text in Exhibit 5 is the strongest evidence that 24X is treating tokenization as a form of the same security.

Under the proposed language, a security may trade in traditional form or, during the DTC pilot, in tokenized form.

A tokenized DTC Eligible Security would be tradable on the same 24X book and with the same execution priority as the traditional version only if it is fungible with the traditional share, has the same CUSIP and trading symbol, and affords the same rights and privileges.

That rights language is important. The filing ties tokenized treatment to the same rights package as the traditional security.

A tokenized instrument that does not carry those rights or share the same CUSIP and symbol would be treated as a separate product rather than a tokenized form of the existing share.

The filing also makes tokenization a controlled preference. Eligible participants that want tokenized settlement would select a designated flag at order entry.

That flag may include DTC-required information, such as the blockchain and wallet address. 24X would communicate the instruction to DTC, but DTC would execute the preference only if it fits DTC’s rules, policies, procedures, and the terms of the no-action letter.

If the member is not eligible, the security is not eligible, the blockchain is not compatible, or the wallet is not registered with DTC, the order remains in traditional form.

That fallback reveals the control point. The token layer is subordinate to DTC eligibility and exchange procedures, not the other way around.

This creates a practical boundary for the whole filing. Tokenized access can exist, but it has to pass through member eligibility, security eligibility, wallet registration, blockchain compatibility, and DTC’s own operating limits.

The more a tokenized product moves away from those controls, the further it strays from the route 24X is asking to use here.

DTC keeps the record layer close for tokenized stocks

The 24X proposal depends on DTC’s tokenization pilot, which rests on a Dec. 11, 2025 SEC staff no-action letter.

That letter describes a pilot version of DTCC Tokenization Services that lets DTC participants elect to record security entitlements to DTC-held securities on a distributed ledger rather than only on DTC’s centralized ledger.

The pilot is participant-based. A DTC participant would register one or more approved blockchain addresses as registered wallets.

If the participant instructs DTC to tokenize an eligible security entitlement, DTC would debit the entitlement from the participant’s account, credit it to a Digital Omnibus Account, and mint a token representing that entitlement to the participant’s registered wallet.

Cede & Co., DTC’s nominee, would remain the registered owner of the underlying securities represented by tokenized entitlements.

DTC would also track token movements through LedgerScan, an off-chain system that monitors wallet activity and serves as DTC’s official books and records for tokenized entitlements.

That architecture gives tokenization some blockchain-like properties while keeping the equity record inside DTC’s controlled environment.

Tokens can move between registered wallets tied to participants, but DTC retains visibility and sets technology standards.

The pilot also includes limits: eligible securities include Russell 1000 securities, U.S. Treasuries, and major-index ETFs; tokenized entitlements receive no collateral or settlement value for DTC risk controls; DTC must report quarterly to SEC staff; and the staff position withdraws three years after launch unless the framework changes.

Those details make the filing more consequential. 24X and DTC are building a controlled path for tokenized access inside the machinery that already sits behind U.S. equity trading.

That controlled path still leaves practical unknowns for the market. 24X has to identify the eligible securities, DTC has to determine which participants, blockchains, and wallets are approved, and the operational value has to become visible to users who may never see the DTC layer directly.

The real tokenized stock contest is distribution

The 24X filing leaves crypto-native venue capture unresolved. It does, however, show that regulated venues are building a compliant route for tokenized stock demand before that competitive question is answered.

The distinction changes the competitive frame because the tokenized-equity story has often been presented as a direct fight between crypto apps and traditional brokers.

Crypto-native platforms can offer global access, familiar wallet interfaces, and always-on user behavior. Products that merely track stock prices or depend on wrappers may still leave holders short of the full rights of a share.

The 24X-DTC model attacks that gap from the other direction. It preserves the rights and market identity of the underlying security, but it does so by keeping access inside exchange and DTC controls.

The tradeoff is clear: the model may feel less open than a crypto-native product, but it keeps the share inside a legal and operational framework familiar to issuers, brokers, regulators, and institutions.

The DTC pilot pattern has already been visible in prior CryptoSlate coverage of the DTC tokenization pilot: tokenization is being introduced through existing custody and settlement rails, with limited eligibility and reporting obligations.

Separate plans from ICE and NYSE point to other incumbent approaches, including a planned tokenized securities platform with always-on and faster-settlement ambitions, but that is distinct from the 24X filing’s DTC-pilot structure.

The immediate signal from SR-24X-2026-20 is a specific compromise: make the access tokenized, but keep the security, the book, the rights, and the settlement controls recognizably Wall Street.

The next test is whether that compromise is useful enough. If DTC-compatible exchange tokenization delivers meaningful after-hours access, global distribution, or operational efficiency without breaking shareholder rights, legacy infrastructure may own the first mainstream version of tokenized equities.

If it feels too permissioned or too hidden from end users, crypto apps will keep pressing the distribution argument.

For now, the route is forming through DTC. Tokenized stocks may arrive with a blockchain reference in the order flow, but the core path still runs through DTC.

The post Centralized Wall Street gatekeepers to control investors’ route into tokenized stocks through old pipes appeared first on CryptoSlate.