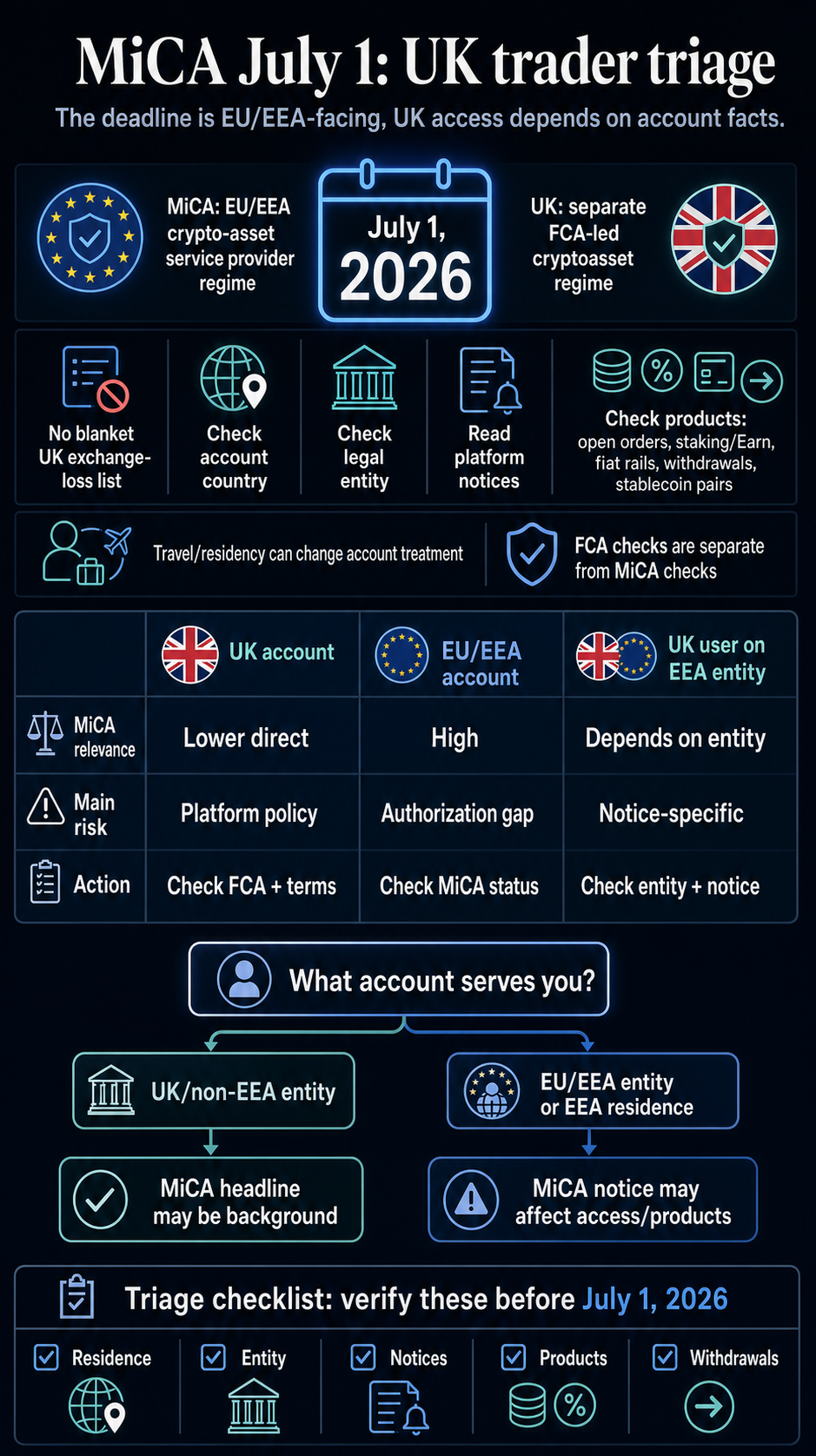

MiCA’s July 1 deadline feels as if it were a Europe-wide exchange shutdown. For UK traders, the direct rulebook remains the UK’s FCA-led regime; the operational risk is that an exchange account may be classified through a different country, legal entity, or product notice.

The same exchange brand can serve customers through different legal entities. A UK user may therefore see a message written for EU clients, miss one that applies to an EEA-linked account, or overlook a product change affecting deposits, yield, open orders, or withdrawals.

The account contract and jurisdiction attached to it carry more weight than the logo on the app.

The European Securities and Markets Authority has warned that the MiCA transitional period ends on July 1, 2026, and that EU clients should check whether their provider is authorized under MiCA or operating under a valid transition.

The UK sits outside that EU regime and is building its own cryptoasset framework through the Financial Conduct Authority and HM Treasury. A blanket list of exchanges that UK traders lose on July 1 would go beyond the sourced record.

What July 1 changes in the EU

MiCA is the EU’s framework for crypto-asset issuance, trading and crypto-asset service providers. ESMA’s MiCA overview describes it as the bloc’s regulatory regime for crypto-assets and related services.

The July 1 date marks the end of the transition period for firms that had been allowed to keep serving EU clients while seeking authorization or using national transitional arrangements.

For an EU client, that can become a hard access question. If a crypto-asset service provider is not authorized and does not have permission to continue operating under transition, the platform may have to stop offering certain services to those clients or wind down its activities.

That is why ESMA has urged clients to check authorization status and why exchange notices across the bloc now carry more operational weight than normal marketing emails.

For a UK resident whose account is clearly served outside the EU/EEA, the same deadline leads to a different analysis. The UK did not import MiCA as its domestic crypto rulebook after Brexit.

UK access questions currently focus on UK-specific registration, financial promotion, and future permission rules, rather than ESMA authorization. The FCA’s new regime page shows that the UK is completing its own regulatory process rather than treating MiCA authorization as the test for UK-facing services.

The practical problem is that users rarely think in legal entities. They think in brands.

An exchange can operate through several entities, serve different countries under different contracts, and apply product rules based on residence, account country, or onboarding route. MiCA is therefore a reason to verify how the account is classified, rather than a direct UK cutoff on its own.

A UK account can still pick up EU-linked risk if the contract, residence record or product notice points in that direction. A user who opened an account while living in the EEA, later moved to the UK, or uses a platform entity that serves European clients may need to read the notice differently from someone onboarded through a UK-specific entity.

The real-world answer starts there: identify the account facts first, then read the deadline through that lens.

Why the same exchange brand can mean different exposure

Binance has become the clearest example of that confusion because it sits at the center of the July 1 social chatter.

CryptoSlate has already covered the EU-focused Binance access and liquidity story, including how the MiCA deadline has put Binance access and USDT liquidity in the spotlight. That earlier coverage supplies background, while the UK question turns on account treatment.

Binance’s own European user update shows why platform changes must be read by country and account status. For a UK trader, the relevant test is whether Binance or any other platform has sent a notice that specifically applies to the user’s account, country or product.

The same account-first test applies to product chatter. Posts may mention spot orders, deposits, staking, Earn products, stablecoin pairs, fiat rails or withdrawals.

Those terms are useful for searching a user’s inbox and app notification center, while the account’s own platform notice determines whether any of them apply. The safer approach is to treat them as possible exposure points that require confirmation in the user’s own notice.

A trader should also separate three questions that are often conflated. First, can the platform serve EU clients after July 1? Second, is the user’s account legally treated as an EU/EEA account, a UK account, or an account in another jurisdiction?

Third, has the platform changed a specific product, such as yield, margin, stablecoin access, deposits, withdrawals, or fiat rails, for that account? The first question is directly about MiCA authorization. The second and third require account-specific evidence.

That distinction keeps the UK question separate from the broader Binance story. Prior CryptoSlate coverage covers the EU access and liquidity stakes.

UK readers need to check whether their account country, legal entity, and product notice match the EU problem described in those stories. If the answer is unclear, the immediate task is to locate the platform’s own message and check whether it names the user’s account category.

The UK regime is a separate check

For UK-only access, the FCA is the relevant regulatory starting point. The FCA’s cryptoasset information for firms covers current UK-facing obligations such as anti-money laundering registration and financial promotion requirements.

Its new-regime materials point to a broader domestic authorization framework still being built. CryptoSlate’s UK regulatory guides have also tracked the separate UK path for cryptoasset activities and permissions, including UK cryptoasset regulations and the FCA-regulated activities regime.

That means a UK trader should treat MiCA status and UK status as separate checks. An exchange may have a MiCA problem in Europe and a different FCA, financial promotion, or business model issue in the UK.

It may also be registered or structured for one type of UK activity while handling another through different terms. Those distinctions are tedious, but they are where account access questions usually live.

The same logic applies when a UK user is traveling or has recently changed residence. A platform may rely on declared residence, verification documents, IP/location controls, local entity terms, or country-specific product restrictions.

None of that turns MiCA into a UK law. It does mean that a user who assumes their account is UK-only without checking the account entity may miss the actual reason a service is being changed.

This simple triage table can reduce the risk of reading the wrong notice:

| Account situation | Likely MiCA relevance | What to check | What to avoid assuming |

|---|---|---|---|

| UK resident with a UK or non-EEA account entity | Lower direct relevance, but platform policy still matters | Account terms, UK entity, FCA status, financial-promotion notices and withdrawals | Every EU headline applies to the account |

| UK resident served through an EU/EEA entity | Potentially higher if the platform treats the account as in-scope for EU changes | Legal entity, onboarding country, MiCA notices, product restrictions and wind-down language | UK residence alone overrides the account contract |

| EU/EEA resident temporarily in the UK | High if the account remains an EU/EEA client account | Residence record, platform communications and whether withdrawals or only new activity are affected | Physical location in the UK changes the account’s regulatory treatment |

| UK user holding a product named in a platform notice | Depends on the account and product | Specific notices for stablecoin pairs, staking/Earn, margin/perps, fiat rails, transfers and custody | Product chatter equals a universal exchange shutdown |

How UK traders should triage July 1 notices

The practical checklist is straightforward, but it has to be account-specific. Start with the account profile, rather than the exchange brand.

Confirm the legal residence and account country on file. Check the legal entity named in the terms of service, app footer, or any recent notice.

Then search emails, app notifications, and support center messages for terms such as MiCA, EU, EEA, UK, withdrawal, transfer, custody, fiat rail, stablecoin, staking, Earn, margin, perps, open order, or account closure.

The next step is to separate access from product exposure. A notice that restricts new orders leaves a different problem from a notice that disables withdrawals.

A staking or Earn wind-down requires a different response from a full account closure. A stablecoin-pair change is separate from losing access to spot trading generally.

Where an exchange says a user is affected, the user should check deadlines, withdrawal windows, conversion options, and whether any open position or yield product needs manual action.

For UK-specific questions, check the FCA separately. That includes whether the firm appears in relevant FCA registration or warning materials, whether communications to UK users comply with financial promotion rules, and whether the platform states that it offers the product to UK residents through a particular entity.

This is regulatory triage, not legal advice.

The July 1 test is account classification, not a universal UK exchange-loss list. The defensible answer is that MiCA should not directly cut off UK residents solely because they are in the UK.

The live risk is that exchange brands, account entities, and product notices do not map neatly onto social media shorthand about the EU deadline. What happens next will depend less on the slogan attached to MiCA and more on whether platforms provide clear, jurisdiction-specific notices before users discover a blocked order, a changed yield product, or a withdrawal route they should have checked earlier.

The post Will UK traders lose crypto exchange access after MiCA’s July 1 deadline? appeared first on CryptoSlate.